What is Home Loan?

What is the Eligibility Criteria for a Home Loan?

What is the tenure of a home loan?

What is a Power Of Attorney?

What is Pre-EMI?

How is the interest rate calculated?

How do I benefit if the interest is calculated on a daily reducing balance

What is a down payment/margin money?

Can I sell the property even when the home loan is outstanding?

What are the types of insurances available with Home Loan?

Can I apply for a joint loan with my friend?

Who can be joint borrowers in home loan?

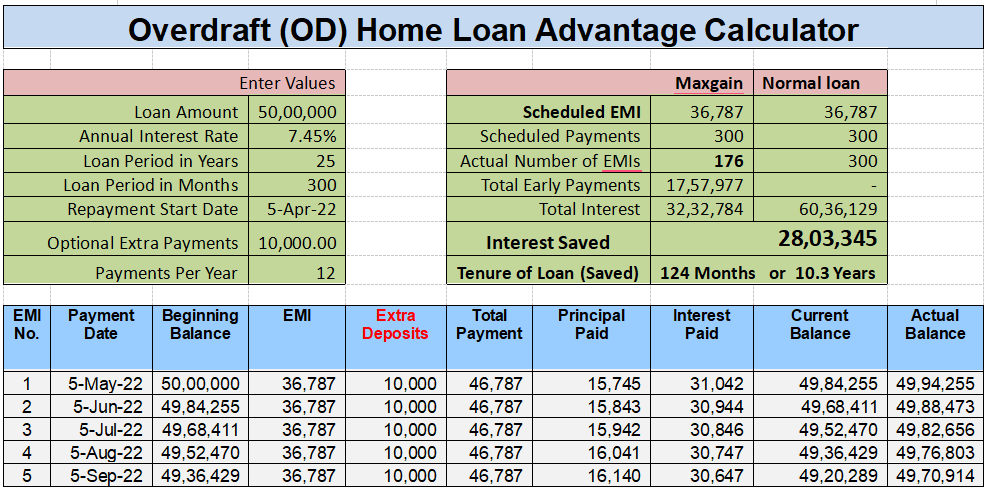

What is the Overdraft (OD) home loan?

What is the maximum number of joint borrowers for a home loan?

What is floating rate home loan?

What is a fixed rate home loan?

Can I switch from a floating rate home loan to a fixed rate?

Should I apply for a home loan with a public or private bank?

What are the charges associated with a home loan process?

What documents do I need to submit with my home loan application?

Is balance transfer of Home Loan with Home Top Up loan permitted?

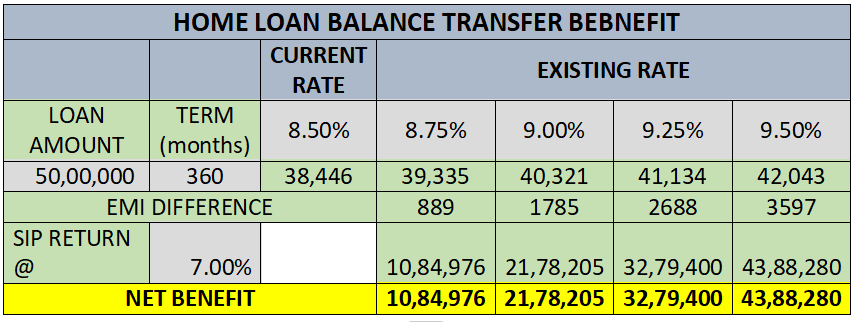

Is there any benefit to balance transfer?

Is there any tax benefit available on home loans?

What is a top up loan?

What costs are not covered in home loan?

How do home loan requirements vary for an apartment and a plot of land?

What is part/subsequent disbursement of a home loan?

When does my home loan EMIs start?

How does your home loan repayment work?

What is PMAY Scheme and how it can benefit Home Loan buyers?

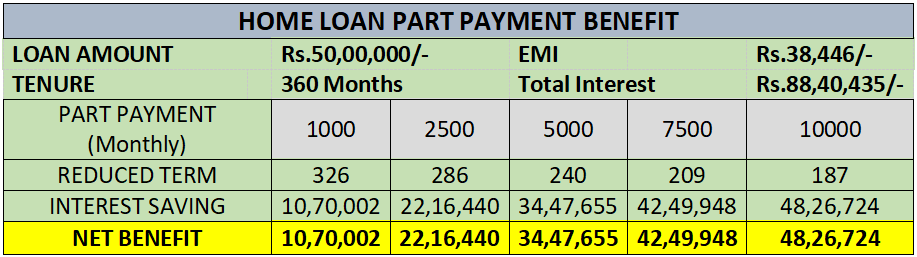

Can I prepay my outstanding housing loan amount?

What is a Loan against Property (LAP)?

Can I balance transfer the Loan against Property (LAP)?

What is maximum funding that I can avail on a property as LAP?

What is the maximum term for which I can avail a Loan against Property (LAP)?

Can I avail Loan against Property (LAP) for a commercial property?